- Transfer pricing is pivotal to Kiribati’s economic landscape, affecting its integration into global trade.

- This financial practice involves setting prices for transactions between multinational corporations’ entities across borders.

- Kiribati must balance traditional practices with international commerce to bolster its development goals.

- The arm’s length principle ensures transactions between related companies mimic those between independent entities.

- Accurate transfer pricing can increase tax revenue for Kiribati, aiding in funding essential services and combating climate change.

- Regulating transfer pricing and joining global initiatives can prevent tax base erosion and profit shifting.

- Active participation in international frameworks like the OECD’s Inclusive Framework on BEPS is crucial for safeguarding Kiribati’s economic interests.

- Properly implemented, transfer pricing can promote sustainable development and economic resilience for Kiribati.

A gentle breeze rustles the palms on Kiribati’s picturesque shores, a stark contrast to the intense tides of globalization influencing its economy. Nestled in the central Pacific Ocean, this small island nation finds itself at the intriguing intersection of local traditions and international commerce. One crucial concept shaping Kiribati’s economic landscape is transfer pricing—a pivotal mechanism in global trade.

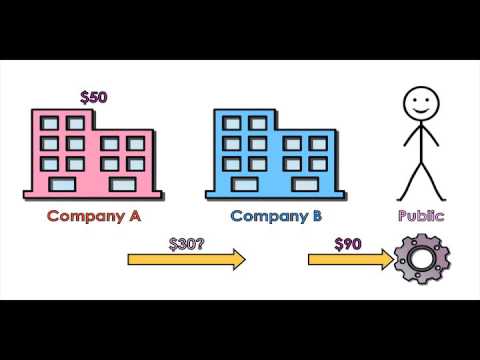

Imagine a vast interconnected web of transactions, where multinational corporations steer their businesses through the ebbs and flows of various tax jurisdictions. Transfer pricing is the practice of setting prices for goods and services exchanged between these related entities, spanning international borders. It is a necessary tool for companies to allocate income and expenses appropriately, ensuring that each branch of a corporation in different parts of the world operates cohesively.

For Kiribati, a nation composed of 33 atolls and reef islands, the impact of transfer pricing is both profound and nuanced. Although it is a small player in the global economy, Kiribati must navigate the complexities of this intricate financial practice to bolster its development goals. Picture Kiribati as a small boat in a vast ocean, carefully adjusting its sails to catch the favorable winds of global trade while avoiding the whirlpools of tax evasion and profit shifting.

Multinational enterprises, often eyeing Kiribati’s strategic location and unspoiled natural beauty, establish branches on the islands. These subsidiaries stand at the forefront of transfer pricing implementation. In doing so, they must adhere to the arm’s length principle. This principle mandates that the transactions between related companies should mimic those that would be agreed upon by unrelated, independent entities in a competitive market.

Why does this matter for Kiribati? Because the tax revenue generated from accurately reported profits allows the government to invest more in essential services, infrastructure, and the fight against the ever-looming threat of climate change. Transfer pricing, when executed transparently and equitably, offers Kiribati a lifeline—a chance to thrive in an era dominated by multinational giants.

When transfer pricing practices slide into the murky waters of manipulation, however, profits magically vanish into low-tax jurisdictions, leaving nations like Kiribati shortchanged. Enforcing stringent regulations and joining international efforts to combat tax base erosion are vital steps Kiribati can take. Entities such as the OECD’s Inclusive Framework on BEPS provide developing nations with the guidelines and resources needed to safeguard their tax bases against aggressive practices.

At its heart, transfer pricing is a balancing act—a dance between adherence to global norms and addressing local needs. For Kiribati, maintaining sovereignty over its taxation policies while engaging in the global conversation on fair practices is imperative. Only through active participation and adaptation can this island nation ensure that the winds of globalization fill its sails in the journey towards sustainable development and economic resilience.

The takeaway is clear: Transfer pricing might sound like a dense economic term, but it holds the power to transform national economies when wielded wisely. For Kiribati, it holds the promise of prosperity amid the vast Pacific expanses—a beacon guiding this unique island nation towards equitable growth on the world stage.

Unlocking the Secrets of Transfer Pricing: Its Impact on Kiribati and Global Trade

Understanding Transfer Pricing and Its Global Implications

Transfer pricing is more than just an economic term; it’s a critical facet of international trade and corporate strategy. At its core, it involves setting prices for transactions within a company across various countries. This is especially crucial for multinational corporations (MNCs) that operate in multiple tax jurisdictions. By adhering to transfer pricing regulations, these corporations ensure that profits are appropriately allocated and that each subsidiary pays taxes reflective of its actual income, as opposed to manipulating prices to shift profits to low-tax jurisdictions.

The Arm’s Length Principle: A Key Component

One of the foundational elements of transfer pricing is the arm’s length principle, which ensures that the financial dealings between related entities within an MNC resemble those between unrelated entities in the open market. This principle is vital in preventing tax evasion and ensuring fair competition.

How Transfer Pricing Affects Kiribati

As a small island nation with a unique strategic location, Kiribati faces a dual challenge: leveraging its position to attract international business while safeguarding its economic integrity from potential tax manipulation. The implementation of proper transfer pricing practices is crucial for Kiribati’s tax revenue, allowing for significant investments in infrastructure, essential public services, and climate change mitigation efforts.

Multinational companies see Kiribati’s potential not only as a business location but also for its natural beauty and resources. However, improper transfer pricing practices could result in the country losing out on significant tax revenues.

Steps for Kiribati to Strengthen Economic Sustainability

1. Alignment with International Standards: Engaging with global bodies like the OECD’s Inclusive Framework on BEPS (Base Erosion and Profit Shifting) can equip Kiribati with the necessary tools to implement stringent transfer pricing regulations.

2. Capacity Building: Investing in building local expertise in international taxation can empower the country to detect and prevent transfer pricing abuses.

3. Legislative Framework: Establishing a robust legal framework can help regulate and monitor transfer pricing activities, ensuring compliance with international norms.

Security, Sustainability, and Economic Predictions

To bolster its economic resilience, Kiribati might consider diversifying its economy to prevent over-reliance on MNCs and foreign investments. Investing in sustainable tourism and renewable energy could provide alternative revenue streams, reducing vulnerability to global trade dynamics.

Actionable Recommendations for Kiribati

– Craft a comprehensive transfer pricing policy aligning with the arm’s length principle and international guidelines.

– Enhance knowledge and skills around international tax issues through partnerships and training programs.

– Implement rigorous audit practices to ensure compliance and deter manipulative transfer pricing activities.

Final Thoughts

Transfer pricing may seem like an intricate financial concept, but for Kiribati, mastering it holds the promise of sustainable economic development. By leveraging global partnerships, investing in capacity building, and enforcing rigorous policies, Kiribati can navigate the challenging waters of globalization to achieve equitable growth.

For further information on transfer pricing and global tax standards, visit the OECD website.