Table of Contents

- Overview of India’s Tax System in 2025

- Key Changes in Direct and Indirect Taxes

- Compliance Requirements and Deadlines

- GST Evolution: Recent Updates and Impact

- Income Tax Slabs and Deductions: What’s New?

- Corporate Tax Trends and Startup Incentives

- Digital Taxation and Cryptocurrency Regulations

- Case Studies: Real Impacts on Individuals and Businesses

- Statistical Highlights from the Ministry of Finance

- Future Outlook: Tax Reforms and Policy Roadmap (2025–2030)

- Sources & References

Overview of India’s Tax System in 2025

India’s tax system in 2025 remains a dual structure comprising direct and indirect taxes, administered primarily by the Income Tax Department and the Central Board of Indirect Taxes and Customs (CBIC). Direct taxes, notably income tax and corporate tax, are levied on individuals and businesses, while indirect taxes, primarily the Goods and Services Tax (GST), apply to the supply of goods and services across the country.

Under the current regime, personal income tax continues to offer taxpayers a choice between the old slab system—allowing various exemptions and deductions—and the newer concessional regime under Section 115BAC, which forgoes most exemptions for lower rates. For Assessment Year 2025-26, the new tax regime is now the default, with slabs starting at 5% for income above ₹3 lakh and peaking at 30% for income above ₹15 lakh, as per Income Tax Department. Corporate tax rates remain at 22% (plus surcharge and cess) for domestic companies not availing incentives, and 15% for new manufacturing companies.

GST, in effect since 2017, has stabilized as the primary indirect tax, subsuming various central and state levies. The GST Council, the apex decision-making body, continues to review rates and compliance requirements, aiming for further simplification and broadening of the tax base. As of 2025, GST collections consistently exceed ₹1.6 lakh crore monthly, reflecting robust compliance and economic recovery (Central Board of Indirect Taxes and Customs).

Compliance is increasingly digitalized. Income tax filing, TDS/TCS payments, and GST returns are all managed through online portals, with e-verification and pre-filled forms aimed at improving taxpayer experience and minimizing errors (Income Tax Department). Enforcement of e-invoicing under GST, now mandatory for businesses with turnover above ₹5 crore, strengthens transparency and curbs evasion (Central Board of Indirect Taxes and Customs).

Key statistics for FY 2023-24 show direct tax collection of over ₹19.58 lakh crore and GST revenue surpassing ₹19.67 lakh crore, indicating a balanced contribution from both tax streams (Ministry of Finance). Looking ahead, policy focus is on rationalizing GST rates and further widening the tax base, with the government targeting increased voluntary compliance and higher digital integration. Reforms such as faceless assessments and ongoing dispute resolution schemes are expected to enhance efficiency and trust in the tax system.

Key Changes in Direct and Indirect Taxes

The Indian tax landscape continues to evolve rapidly as the government focuses on broadening the tax base, simplifying compliance, and promoting economic growth. In the fiscal year 2025, several key changes have been introduced in both direct and indirect taxes, reflecting policy priorities and the need for robust revenue collection.

Direct Taxes

- Personal Income Tax: The Finance Act, 2024 maintained the new concessional tax regime as the default for individual taxpayers, with unchanged slab rates for FY 2024-25. The regime continues to offer lower rates but fewer exemptions and deductions. Taxpayers may still opt for the old regime with existing allowances. The government also increased the threshold for presumptive taxation for professionals to Rs. 75 lakh, provided 95% of receipts are digital, further incentivizing digital transactions Central Board of Direct Taxes.

- Corporate Tax: The concessional corporate tax rate of 15% for new manufacturing companies incorporated before March 31, 2024, has not been extended. Companies now incorporated after this date revert to the standard rates. The surcharge on certain income categories has been rationalized to reduce the overall tax burden on high-value transactions Central Board of Direct Taxes.

- TDS and Compliance: New provisions mandate increased reporting and compliance, particularly for digital transactions and high-value payments. The government is leveraging technology through its Annual Information Statement (AIS) and e-verification to improve compliance and detect non-reporting Central Board of Direct Taxes.

Indirect Taxes

- Goods and Services Tax (GST): GST rates have remained stable overall, but the government continues to rationalize rates on select goods and services. E-invoicing is now mandatory for businesses with turnover exceeding Rs. 5 crore, bolstering transparency and minimizing tax evasion Goods and Services Tax Council.

- Customs Duties: The Union Budget 2024-25 proposed selective increases and reductions in customs duties to encourage domestic manufacturing and align with Make in India objectives. Duty on key components in electronics and renewable energy sectors has been rationalized Central Board of Indirect Taxes and Customs.

- Compliance Measures: The use of artificial intelligence and data analytics by tax authorities is set to intensify, with stricter scrutiny of input tax credit (ITC) claims and cross-verification of returns Central Board of Indirect Taxes and Customs.

Outlook

With a focus on digitalization and transparency, the government is expected to further streamline tax administration and widen the tax net in the coming years. Continued enhancements in compliance technology are likely, alongside incremental policy adjustments to support economic priorities and revenue targets.

Compliance Requirements and Deadlines

India’s tax compliance landscape in 2025 is governed primarily by the Income Tax Act, 1961 and the Goods and Services Tax (GST) regime under the Central Goods and Services Tax Act, 2017. Both direct (income tax) and indirect (GST) taxes require strict adherence to filing schedules and procedural mandates.

- Income Tax Compliance: For Assessment Year (AY) 2025-26, individual taxpayers (other than those subject to audit) must file their income tax returns (ITR) by July 31, 2025. Businesses and professionals requiring audit must file by October 31, 2025. Taxpayers subject to transfer pricing provisions have until November 30, 2025 to file. Delays attract late fees under Section 234F and potential interest on unpaid taxes (Income Tax Department).

- Advance Tax: Individuals and companies with tax liability exceeding ₹10,000 in a financial year must pay advance tax in four instalments: June 15, September 15, December 15, and March 15, as per Section 211. Non-compliance leads to interest liabilities under Sections 234B and 234C (Income Tax Department).

- Tax Deducted at Source (TDS) and Tax Collected at Source (TCS): Entities deducting TDS/TCS must deposit amounts monthly (by the 7th of the following month) and file quarterly returns (Form 24Q, 26Q, 27Q, etc.) within prescribed timelines. Certificate issuance (Form 16/16A) deadlines also apply (Protean (formerly NSDL), TDS Central Processing Cell).

- GST Compliance: Registered taxpayers must file monthly GSTR-1 (outward supplies) by the 11th and GSTR-3B (summary return) by the 20th of the following month. Quarterly filers (under QRMP scheme) have alternative deadlines. Annual GST return (GSTR-9) for FY 2024-25 is due by December 31, 2025. Non-compliance attracts late fees and interest (Goods and Services Tax Council).

- Revised and Belated Returns: Revised or belated ITRs for AY 2025-26 can be filed up to December 31, 2025 or before completion of assessment, whichever is earlier (Income Tax Department).

- Statutory Audit and Reporting: Companies and firms crossing specified turnover must complete statutory audits and submit tax audit reports (Form 3CA/3CB & 3CD) by September 30, 2025 (The Institute of Chartered Accountants of India).

With the government’s ongoing digitization drive and increasing use of analytics for compliance assessment, stricter enforcement and automated notices are expected in 2025 and beyond. Taxpayers are advised to regularly check official portals for updates and adhere to evolving requirements.

GST Evolution: Recent Updates and Impact

The Goods and Services Tax (GST) in India, implemented in July 2017, marked a significant transformation in the country’s indirect tax landscape by subsuming multiple state and central taxes into a unified structure. Since its inception, GST has undergone continuous evolution, with notable updates and policy shifts, particularly as the government aims to streamline compliance and enhance revenue in the years leading up to 2025.

In 2024 and moving into 2025, the GST Council has continued to play a pivotal role in guiding changes to the GST regime. Key recent developments include rationalization of tax rates on several goods and services, expansion of the e-invoicing mandate to businesses with lower turnover thresholds, and ongoing improvements in the GSTN (Goods and Services Tax Network) portal to facilitate more efficient return filing and data reconciliation.

One of the major compliance updates is the enhancement of the e-invoicing system. Effective from August 2023, the threshold for mandatory e-invoicing was reduced to Rs. 5 crore in aggregate turnover, aiming to bring more businesses under real-time invoice reporting and curb tax evasion. This threshold is expected to be further lowered as the government targets universal e-invoicing by 2025, which will significantly increase transparency and automate tax credit matching (Goods and Services Tax Network).

Rate rationalization remains on the agenda. In its 50th and subsequent meetings, the GST Council has discussed merging the 12% and 18% slabs into a single rate to simplify the structure, though implementation is still pending. Such changes are expected to reduce classification disputes and litigation, making compliance easier for businesses (Press Information Bureau, Government of India).

Compliance has become more data-driven, with the introduction of artificial intelligence and analytics to detect mismatches in Input Tax Credit (ITC) claims and curb fraudulent practices. The introduction of pre-filled returns based on supplier filings is being piloted, which is expected to ease the compliance burden for small and medium enterprises (SMEs) (Central Board of Indirect Taxes & Customs).

Key statistics reflect steady growth in GST collections. As of early 2024, monthly gross GST revenue collections have consistently exceeded Rs. 1.5 lakh crore, with the trend projected to continue in 2025 due to improved compliance and a broader base. The government’s focus is now on streamlining dispute resolution and introducing a comprehensive GST Appellate Tribunal, expected to be operational by 2025, to resolve pending cases efficiently (Ministry of Finance, Government of India).

Looking ahead, GST in India is poised for further digital transformation, tighter compliance frameworks, and a more simplified rate structure. These changes aim to boost ease of doing business, increase tax buoyancy, and minimize litigation, solidifying the GST regime as a cornerstone of India’s tax system through 2025 and beyond.

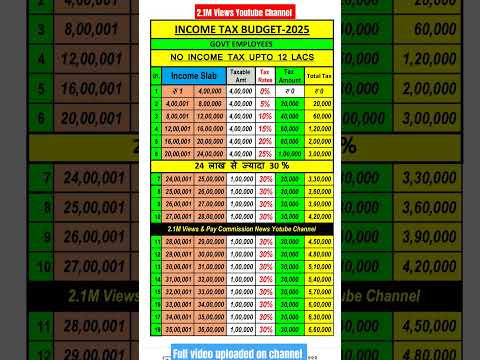

Income Tax Slabs and Deductions: What’s New?

The financial year 2024-25 marks significant developments in India’s income tax regime, impacting both individual taxpayers and businesses. The most notable change is the continued emphasis on the “new tax regime” under section 115BAC of the Income Tax Act, which the government has positioned as the default tax regime from Assessment Year (AY) 2024-25 onwards. Taxpayers may still opt for the old regime, which offers various exemptions and deductions, but must exercise this choice explicitly in their tax return or via Form 10-IEA for those with business income. The new regime features simplified, lower tax rates but eliminates most deductions and exemptions (Income Tax Department).

-

Revised Slabs (FY 2024-25, AY 2025-26):

The new regime’s tax slabs are as follows:- Up to ₹3 lakh: Nil

- ₹3,00,001 to ₹6,00,000: 5%

- ₹6,00,001 to ₹9,00,000: 10%

- ₹9,00,001 to ₹12,00,000: 15%

- ₹12,00,001 to ₹15,00,000: 20%

- Above ₹15,00,000: 30%

(Income Tax Department)

-

Rebate and Standard Deduction:

The section 87A rebate remains available for income up to ₹7 lakh under the new regime, ensuring no tax liability for those below this threshold. For salaried individuals and pensioners, a standard deduction of ₹50,000 is now permitted under the new regime as well (Income Tax Department). -

Changes to Deductions and Exemptions:

The new regime disallows most deductions (e.g., under sections 80C, 80D, HRA, LTA), aiming to simplify compliance. However, certain deductions like employer’s contribution to NPS (section 80CCD(2)) and voluntary retirement (section 10(10C)) remain available (Income Tax Department). -

Compliance and Outlook:

Taxpayers must now carefully evaluate which regime is more beneficial each year, considering the loss of deductions versus lower rates. The Central Board of Direct Taxes (CBDT) continues to digitize and streamline return filing, with pre-filled returns and e-verification becoming the norm (Central Board of Direct Taxes). In the coming years, further rationalization toward fewer exemptions and increased digital compliance is expected, aligning with the government’s stated goal of a more transparent tax environment.

Corporate Tax Trends and Startup Incentives

India’s corporate tax environment has undergone significant transformation in recent years, with a focus on stimulating investment, simplifying compliance, and supporting the startup ecosystem. For the assessment year 2025–26 and beyond, policy continuity and incremental reforms are anticipated.

Corporate Tax Rates and Regime Changes

India currently offers a concessional corporate tax rate of 22% (plus applicable surcharge and cess) for domestic companies that do not claim specified exemptions and incentives, as per Section 115BAA. For new manufacturing companies incorporated after October 1, 2019 and commencing production before March 31, 2024, a lower rate of 15% is available under Section 115BAB. The base corporate tax rate for other domestic companies remains at 30% (Income Tax Department).

The government, in its Union Budget for 2024–25, has signaled stability in tax rates, aiming to foster a predictable tax regime for businesses. No major changes to corporate tax rates or surcharges have been proposed for FY 2024–25, reinforcing investor confidence. However, a continued rationalization of tax compliance procedures, including faceless assessments and appeals, is expected to further streamline processes (Central Board of Direct Taxes).

Startup Incentives and Compliance

The Indian government continues to bolster its flagship Startup India initiative, offering tax incentives to eligible startups. Section 80-IAC of the Income Tax Act allows eligible startups incorporated between April 1, 2016 and March 31, 2025 to claim a 100% tax deduction on profits for three consecutive years out of ten since incorporation. The eligibility window was extended in Budget 2024 to further support the ecosystem (Income Tax Department).

Startups also benefit from exemption on angel tax (Section 56(2)(viib)) for investments from notified investors and DPIIT-recognized startups, addressing concerns over valuation-related tax liabilities (Department for Promotion of Industry and Internal Trade). Mandatory compliance, however, includes annual filings, documentation for recognition, and adherence to prescribed conditions.

Key Statistics and Outlook

Corporate tax collection for FY 2023–24 reached a record ₹9.57 lakh crore, underscoring robust profitability and formalization in the sector (Press Information Bureau). The proportion of startup registrations continues to grow, with over 1.2 lakh DPIIT-recognized startups as of early 2024. Looking ahead, the government is expected to maintain favorable tax policies for corporates and startups, focusing on digital compliance, ease of doing business, and targeted incentives to catalyze private sector growth.

Digital Taxation and Cryptocurrency Regulations

India’s approach to digital taxation and cryptocurrency regulation continues to evolve rapidly in 2025, reflecting both domestic priorities and international trends. The government has been intensifying efforts to tax digital transactions and regulate the burgeoning crypto sector, aiming to boost revenue and ensure financial stability.

Digital Taxation: The Equalisation Levy, introduced in 2016 and expanded in 2020 to cover e-commerce operators, remains a cornerstone of India’s digital tax regime. As of 2025, a 2% levy applies to gross revenues earned by non-resident e-commerce companies from Indian users. These provisions target global digital giants lacking physical presence in India. The government, through the Income Tax Department, continues to clarify scope and compliance, especially in light of evolving international consensus on digital taxation under the OECD/G20 Inclusive Framework.

- Equalisation Levy collections have shown a steady rise, with the Press Information Bureau reporting over ₹4,000 crore collected for FY 2023-24, and expectations for further growth as digital commerce expands.

- The government has signaled willingness to revisit digital tax measures in line with a multilateral solution if the OECD Pillar One agreement is finalized and implemented.

Cryptocurrency Regulations: Since 2022, India has imposed a 30% tax on gains from the transfer of “virtual digital assets” (VDAs), including cryptocurrencies and NFTs, along with a 1% Tax Deducted at Source (TDS) on transfers above prescribed thresholds. These rules, administered by the Central Board of Direct Taxes (CBDT), require crypto exchanges and traders to maintain detailed records and file returns accordingly.

- The government’s recent budget proposals reaffirmed the existing regime, with no relief on tax rates or TDS, signaling a continued cautious stance.

- The Ministry of Finance has emphasized investor protection, anti-money laundering compliance, and robust reporting as priorities, with ongoing consultations on a possible comprehensive legislative framework.

- Crypto-related tax collections remain modest relative to expectations, with formal sector participation limited due to high tax rates and regulatory uncertainty.

Outlook (2025 and Beyond): India’s digital taxation framework is expected to remain dynamic, with possible alignment to global standards once international agreements crystallize. For cryptocurrencies, the current tax and compliance regime is likely to persist in the near term, although a specific regulatory bill may emerge. Businesses and investors should monitor updates from the Ministry of Finance and the Income Tax Department for changes in law, compliance obligations, and enforcement trends as India balances innovation with regulation in the digital economy.

Case Studies: Real Impacts on Individuals and Businesses

India’s tax landscape continues to evolve, directly impacting individuals and businesses through legislative updates, compliance requirements, and enforcement actions. The 2024-2025 fiscal year features several noteworthy case studies reflecting how policy and administration shape real-world outcomes.

- Faceless Assessment and Individual Taxpayers: The faceless assessment regime under the Income Tax Act, 1961, has significantly transformed the experience of individual taxpayers. For instance, in FY 2024-25, a salaried individual in Bengaluru received an intimation under Section 143(1) due to mismatches in Form 26AS and the filed return. The taxpayer resolved the discrepancy through the e-Proceedings portal, illustrating how digitalization has streamlined compliance and reduced physical interface, thus minimizing corruption and arbitrariness. This case typifies the government’s push for transparency and taxpayer convenience (Income Tax Department).

- MSMEs and GST Compliance: Micro, Small, and Medium Enterprises (MSMEs) are significantly impacted by Goods and Services Tax (GST) compliance. In 2025, a textile manufacturer in Surat faced a temporary business disruption due to delayed GST return filings, resulting in suspension of GST registration and disruption in input tax credit flow. Intervention via the GST grievance redressal mechanism and subsequent compliance restored business operations. This illustrates the critical importance of timely GST compliance and the role of digital portals in resolving business issues (Goods and Services Tax Council).

- Multinational Corporations and Transfer Pricing: A global IT company in Hyderabad underwent a transfer pricing audit for the 2022-23 assessment year, leading into a 2025 settlement. The company faced significant adjustments and penalties due to inadequate documentation and benchmarking for inter-company transactions. After presenting revised documentation and engaging with the Dispute Resolution Panel, penalties were reduced. This case highlights ongoing scrutiny of cross-border transactions and the need for robust transfer pricing compliance (Central Board of Direct Taxes).

- High Net Worth Individuals and TDS: A prominent real estate investor was subject to a tax survey under Section 133A in 2025 for alleged non-deduction of Tax Deducted at Source (TDS) on rental income paid to non-residents. The case was resolved after retrospective deduction and payment of TDS, along with interest. This underscores the increasing focus on high-value transactions and cross-border compliance requirements (Income Tax Department).

These examples demonstrate that the Indian tax ecosystem in 2025 is marked by increased digitalization, real-time compliance monitoring, and targeted enforcement—trends expected to intensify as authorities leverage technology and data analytics in upcoming years.

Statistical Highlights from the Ministry of Finance

The Ministry of Finance plays a pivotal role in shaping and monitoring the tax landscape in India, providing detailed statistical data on tax collections, compliance levels, and fiscal trends. For the financial year 2024-25, India’s tax collections have continued their upward trajectory, reflecting both heightened economic activity and improved compliance measures. According to provisional data released by the Ministry of Finance, gross tax revenue for the Union Government is projected to surpass ₹38 lakh crore in FY 2024-25, up from ₹33.61 lakh crore in FY 2023-24, representing robust double-digit growth.

- Direct Taxes: The Central Board of Direct Taxes (CBDT) reported that net direct tax collections (corporate tax and personal income tax) for April-February 2024 stood at ₹16.68 lakh crore—an increase of over 17% compared to the same period in the previous year. For FY 2024-25, direct taxes are expected to contribute over 53% of total gross tax revenue.

- Indirect Taxes: The Central Board of Indirect Taxes and Customs (CBIC) indicated that Goods and Services Tax (GST) collections have consistently crossed the ₹1.5 lakh crore mark per month in 2024. The average monthly gross GST collection during April-February 2024 was approximately ₹1.68 lakh crore, with the annual GST revenue targeted at ₹20.14 lakh crore for FY 2024-25.

- Tax-to-GDP Ratio: The tax-to-GDP ratio, a key indicator of fiscal strength, is estimated to reach 11.7% in 2024-25, according to the Union Budget documents. This marks an improvement from the 11.4% recorded in 2023-24.

- Digitalization and Compliance: The ongoing adoption of digital tax administration tools, such as faceless assessments and e-invoicing, has contributed to better compliance and reduced evasion, as highlighted in recent updates by the Income Tax Department.

- Outlook: The Ministry anticipates sustained growth in tax revenues in the coming years, driven by formalization of the economy, expansion of the tax base, and continued reforms in tax administration.

Overall, these statistical highlights underscore the government’s focus on strengthening revenue mobilization while leveraging technology to enhance transparency and taxpayer services. For the latest and detailed statistical releases, stakeholders are encouraged to consult the Ministry of Finance and its associated departments.

Future Outlook: Tax Reforms and Policy Roadmap (2025–2030)

India’s tax regime is undergoing significant transformation as the country aligns its fiscal policies with evolving economic priorities. The period from 2025 to 2030 is poised for further tax reforms, driven by the need for simplicity, efficiency, and growth stimulation. The Union Budget 2024-25 continued the recent trend of focusing on stability and incremental changes, while signaling intent for deeper reforms in the medium term. Key legislative and policy developments are expected to shape the future of direct and indirect taxation in India.

- Direct Tax Reforms: There is sustained momentum to rationalize personal and corporate income tax structures. The government’s stated aim is to make direct taxes “simpler and more predictable,” potentially through further reduction in tax rates, broadening the base, and phasing out exemptions. The new tax regime with lower rates and fewer deductions is set to be further incentivized, gradually emerging as the default system. Technology-driven compliance—such as faceless assessments and robust e-filing—will become even more prevalent, enhancing transparency and reducing litigation. The Direct Tax Code, though still under consideration, may see renewed attention for codifying and modernizing income tax law by 2030 (Central Board of Direct Taxes).

- Goods and Services Tax (GST): Since its launch, GST has witnessed regular rationalization, and the GST Council is expected to continue refining rate structures and compliance norms through 2025–2030. Discussions are ongoing regarding merging the 12% and 18% slabs and bringing petroleum products under GST. The government is also focused on using AI and big data for compliance monitoring, plugging leakages, and expanding the tax base. With GST collections consistently rising—monthly revenues averaged ₹1.5 lakh crore in early 2025—further simplification is anticipated to support economic formalization (GST Council).

- International Taxation and Digital Economy: As cross-border digital transactions increase, India may refine its approach to taxation of the digital economy, aligning with global initiatives under the OECD/G20 Inclusive Framework. The Equalisation Levy and changes in nexus rules could be further adapted to new business models (Income Tax Department, Ministry of Finance).

- Compliance and Technology: Automation, AI-based risk profiling, and blockchain for e-invoicing are likely to become central to tax administration. Government initiatives like the “Transparent Taxation” platform will further ease compliance and minimize taxpayer interface (Income Tax Department).

Overall, India’s tax policy roadmap from 2025 to 2030 points toward greater digitization, base broadening, and simplification, aiming to foster compliance, investment, and sustainable revenue growth.