Table of Contents

- Executive Summary: The State of Tax Law in Iran (2025)

- Key Regulatory Bodies and Legal Framework

- Major Tax Reforms Effective from 2025

- Corporate Tax: New Rates, Rules, and Compliance Essentials

- Personal Income Tax: Bracket Updates and Filing Changes

- Value Added Tax (VAT) and Indirect Tax Amendments

- Enforcement, Penalties, and Audit Trends

- Sector-Specific Impacts: Energy, Technology, and Startups

- Future Outlook: Projected Reforms Through 2029

- Official Resources and Guidance for Compliance (e.g., intamedia.ir, tax.gov.ir)

- Sources & References

Executive Summary: The State of Tax Law in Iran (2025)

The landscape of tax law in Iran is undergoing significant transformation as the government intensifies efforts to modernize tax administration and improve compliance. As of 2025, these reforms are primarily driven by fiscal needs, ambitions to diversify state revenues, and commitments to transparency and digitalization. The Iranian tax system is governed primarily by the Iranian National Tax Administration (INTA), which administers the Direct Taxation Act, Value Added Tax (VAT) Law, and various sector-specific regulations.

In recent years, the Iranian legislature has enacted amendments to streamline tax processes, address tax evasion, and broaden the tax base. Notably, the 2023 amendments to the Direct Taxation Act introduced stricter reporting obligations, enhanced third-party information exchange, and expanded the use of electronic tax filing platforms. These reforms are expected to bolster transparency and reduce opportunities for underreporting and tax avoidance. The government continues to prioritize digital transformation, with the INTA accelerating the rollout of its integrated tax management system, aiming for full nationwide implementation by 2026 Iranian National Tax Administration.

Key statistics underscore the urgency of these reforms. In the fiscal year ending March 2024, tax revenues accounted for roughly 45% of the national budget, marking a steady increase from prior years as sanctions pressure has constrained oil revenues. The INTA reported a year-on-year growth of over 30% in tax collections, attributed largely to improved compliance measures and expansion of VAT coverage Iranian National Tax Administration. VAT, currently set at 9%, remains a central pillar, with ongoing discussions about potential rate adjustments and exemptions to optimize revenue without stifling economic activity.

- Compliance: Taxpayers face heightened scrutiny, with enforcement actions—including audits and penalties—becoming more frequent. The expansion of electronic invoicing and banking data integration has empowered tax authorities to detect non-compliance more effectively.

- Outlook: For 2025 and the coming years, the government is expected to further tighten compliance requirements, extend digital platforms, and potentially introduce targeted tax incentives to stimulate investment and employment in key sectors. Legislative proposals for incorporating global anti-evasion standards and enhancing cross-border tax cooperation are also under review.

In summary, tax law in Iran in 2025 is characterized by rapid modernization, stricter compliance frameworks, and a growing emphasis on digital solutions. These developments reflect broader economic and fiscal strategies aimed at ensuring sustainable government revenues in a challenging international environment.

Key Regulatory Bodies and Legal Framework

Iran’s tax system is governed by a centralized framework, primarily overseen by the Iranian National Tax Administration (INTA), which operates under the Ministry of Economic Affairs and Finance. The INTA is responsible for tax collection, enforcement, audits, and interpreting tax laws. Its mandate includes both direct and indirect taxes, with a focus on improving compliance, digitalization, and reducing tax evasion.

The core legal instrument is the Direct Taxes Act, which has undergone several amendments to address economic changes and align with global best practices. The act covers individual and corporate income tax, with rates and exemptions updated periodically. Other pivotal legislation includes the Value Added Tax Act and sector-specific tax provisions. These laws are supplemented by executive regulations and circulars issued by the INTA, which further clarify compliance requirements and procedural details.

- Direct Taxes: The Direct Taxes Act governs taxation of individuals, companies, partnerships, and foreign entities with Iranian-source income. Corporate tax rate remains at 25% for 2025, with specific incentives for export-oriented and knowledge-based companies.

- Indirect Taxes: The Value Added Tax (VAT) regime has been gradually expanded, with the standard rate set at 9% as of 2025. Certain goods and services remain exempt or subject to reduced rates to support key economic sectors.

- International Taxation: Iran has bilateral tax treaties with over 40 countries to prevent double taxation and fiscal evasion, administered and negotiated by the Ministry of Economic Affairs and Finance.

Enforcement and dispute resolution are managed by specialized tax courts and committees under the supervision of the Judiciary of the Islamic Republic of Iran. Taxpayers can appeal assessments and penalties through these administrative and judicial channels.

Recent years have seen a push towards digital transformation, including the rollout of the Comprehensive Tax System to streamline filings and increase transparency. Compliance rates are projected to rise as electronic invoicing and data integration become mandatory for more sectors by 2025 and beyond (Iranian National Tax Administration).

Looking ahead, the regulatory landscape is expected to evolve further, with ongoing amendments anticipated to modernize tax law, broaden the tax base, and enhance collection efficiency in line with national development goals.

Major Tax Reforms Effective from 2025

Iran has embarked on significant tax reforms effective from 2025, aiming to expand the tax base, boost government revenues, and improve compliance through modernization and digitalization efforts. This overhaul aligns with broader economic strategies to reduce dependency on oil revenues and foster fiscal sustainability.

A central feature of the 2025 reforms is the full-scale implementation of the Comprehensive Tax Plan (“Tarh-e Jame’ei Maliyati”). The plan mandates the completion and nationwide rollout of the Integrated Tax System (ITS), which unifies taxpayer data, automates tax processes, and enhances information sharing among government agencies. The Iranian National Tax Administration (INTA) now requires all businesses and self-employed individuals to register through electronic portals, submit returns digitally, and utilize e-invoicing for all commercial transactions. This is expected to significantly reduce tax evasion and improve transparency, with the INTA reporting a substantial increase in digital filings during pilot phases in 2023–2024 (Iranian National Tax Administration).

Another major change is the adjustment of tax brackets and rates for both personal and corporate income. The 2025 tax law introduces more progressive personal income tax brackets, with higher rates for top earners and modest relief for lower-income taxpayers. For corporations, while the standard rate remains at 25%, new provisions grant temporary tax incentives for knowledge-based startups and export-oriented companies, aiming to stimulate innovation and non-oil exports (Ministry of Economic Affairs and Finance).

The Value Added Tax (VAT) regime has also been revised. The standard VAT rate stays at 9%, but the 2025 law expands the list of taxable goods and services, while narrowing exemptions and introducing stricter input credit rules. This is designed to curb tax avoidance schemes and increase VAT collections, which represented over 35% of total tax revenue in the previous fiscal year (Iranian National Tax Administration).

To enforce compliance, the reforms introduce robust penalties for non-filing, underreporting, and non-compliance with digital requirements. The INTA has also been granted broader audit powers, including real-time data access from financial institutions and the ability to cross-check transactions with the Customs Administration and Social Security Organization databases.

Looking ahead, Iranian authorities project that these reforms will increase the tax-to-GDP ratio from the current 7.5% to over 10% by 2027, moving closer to regional averages and providing more stable public finances (Ministry of Economic Affairs and Finance). Continued digitalization and targeted incentives are expected to further modernize Iran’s tax environment in the coming years.

Corporate Tax: New Rates, Rules, and Compliance Essentials

The Iranian corporate tax regime has seen notable adjustments in recent years, with the government implementing new rates, rules, and compliance measures aimed at broadening the tax base and enhancing revenue collection. For the 2025 fiscal year, the standard corporate income tax (CIT) rate remains at 25% of taxable profits, applicable to all legal entities except those specifically exempted by law. However, policymakers have signaled ongoing efforts to refine taxation rules in line with economic priorities and global standards.

In terms of tax incentives, certain sectors such as manufacturing, knowledge-based enterprises, and export-oriented businesses continue to benefit from reduced rates or tax holidays, subject to meeting prescribed criteria. For example, companies investing in underdeveloped regions or engaging in high-tech activities may qualify for up to 80% tax exemption for a period of 4-10 years, according to the most recent guidance from the Iranian National Tax Administration. These incentives are part of a broader strategy to stimulate economic growth and employment in targeted sectors.

Compliance requirements have become increasingly stringent. All corporations must file annual tax returns within four months of their fiscal year-end and are required to maintain detailed accounts and supporting documentation for a minimum of 10 years. Electronic filing is now mandatory, and the Iranian National Tax Administration has upgraded its digital platforms to facilitate e-filing and real-time reporting. Non-compliance, late submission, or understatement of income can trigger penalties ranging from 10% to 30% of the unpaid tax, with potential criminal liability in cases of deliberate evasion.

Audit procedures have also been modernized. The tax authority increasingly uses risk-based selection methods, leveraging data analytics to identify discrepancies and target high-risk taxpayers. Cross-border transactions are under heightened scrutiny, particularly with respect to transfer pricing and anti-avoidance measures. The adoption of international standards, including elements of the OECD’s Base Erosion and Profit Shifting (BEPS) framework, is ongoing but not yet fully aligned.

According to the Ministry of Economic Affairs and Finance, corporate tax collection contributed approximately 25% of total tax revenues in the most recent fiscal year, with ongoing reforms expected to increase this share. Looking ahead, Iran is likely to continue tightening enforcement and refining rules to combat evasion, improve transparency, and support fiscal sustainability. Companies operating in Iran should closely monitor legislative updates and ensure robust internal compliance mechanisms to navigate the evolving tax environment through 2025 and beyond.

Personal Income Tax: Bracket Updates and Filing Changes

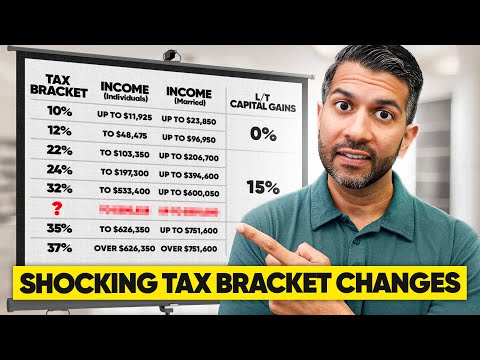

In 2025, Iran’s personal income tax (PIT) regime continues to evolve as the government implements reforms aimed at broadening the tax base and increasing compliance. The most significant legislative update came with the ratification of amendments to the Direct Taxation Act (DTA), which governs the administration and collection of PIT. The Ministry of Economic Affairs and Finance (MEAF) published revised tax brackets effective for the fiscal year 1403 (March 2024–March 2025), reflecting inflation adjustments and the government’s intention to enhance progressivity in the tax system.

- Bracket Structure: For 2025, the annual income exemption threshold has been raised to IRR 120 million. Income up to this amount remains tax-free. Beyond this, progressive rates apply: 10% on the next IRR 360 million, 15% on the following IRR 480 million, 20% on the next IRR 1.08 billion, and a top marginal rate of 25% for income exceeding IRR 2.04 billion. These updates are aimed at providing relief to lower-income earners while taxing higher incomes more substantially (Iran National Tax Administration).

- Filing and Compliance: The government has prioritized digitalization of tax administration. In 2025, all individuals subject to PIT—including employees, self-employed professionals, and business owners—are required to file tax returns electronically via the INTA’s integrated tax system. New features include pre-filled tax forms for employees and enhanced tools for verification of deductions and credits. The filing deadline is set for the end of Khordad (June 20), with late submissions subject to penalties (Iran National Tax Administration).

- Compliance Initiatives: The government has intensified efforts to curb tax evasion, including the cross-referencing of taxpayer data with financial institutions and other governmental databases. Penalties for non-compliance have been increased, and the INTA has expanded its audit capacity in sectors with historically low compliance rates (Ministry of Economic Affairs and Finance).

- Key Statistics: According to official figures, the number of personal income tax filings increased by 18% in 2024, with a compliance rate now surpassing 85%. The government’s target for 2025 is to bring this figure above 90% as digital systems mature (Iran National Tax Administration).

- Outlook: Looking ahead, Iran is expected to further refine tax brackets to keep pace with inflation and economic changes. Additional reforms under discussion include expanding the range of deductible expenses and introducing targeted tax credits to stimulate workforce participation and investment (Iran National Tax Administration).

Value Added Tax (VAT) and Indirect Tax Amendments

Iran’s value added tax (VAT) regime, established under the VAT Act of 2008, has undergone significant amendments in recent years, culminating in further revisions effective for the 2025 fiscal year. These changes reflect the government’s efforts to modernize indirect taxation, close compliance gaps, and align with evolving economic priorities.

The standard VAT rate in Iran remains at 9%, encompassing a 6% national VAT and a 3% provincial tax. However, the Iranian National Tax Administration (INTA) has expanded the scope of taxable goods and services, reducing exemptions and increasing enforcement. Notably, the 2022 amendment to the VAT Act, which continues to shape 2025 practice, brought digital services and e-commerce transactions into the VAT net for the first time, obligating both domestic and foreign digital service providers to register and remit VAT on sales to Iranian consumers.

Key compliance measures implemented by INTA include mandatory use of online sales and purchase invoice platforms, electronic filing of VAT returns, and real-time reporting requirements for businesses above certain annual turnover thresholds. The 2025 fiscal year will see stricter penalties for late or inaccurate VAT filings, alongside enhanced audit frequency targeting high-risk sectors such as construction, telecom, and digital platforms (Iranian National Tax Administration).

Exemptions remain for essential goods such as basic foodstuffs, unprocessed agricultural products, and certain medical services. However, the list of exempt items has been narrowed, especially for luxury goods and non-essential imports, as part of efforts to boost domestic production and revenue. According to the Ministry of Cooperatives, Labour, and Social Welfare, these VAT adjustments are intended to support social welfare programs by increasing fiscal resources.

- In 2023–2024, VAT accounted for over 35% of Iran’s total tax revenue, with a projected increase in 2025 due to broader coverage and improved compliance measures (Iranian National Tax Administration).

- The number of VAT registrants surpassed 1.2 million entities by early 2024, reflecting expanded enforcement and digital economy inclusion (Iranian National Tax Administration).

Looking ahead, Iran’s VAT system is set to become more digitized and integrated with customs and banking data, further reducing opportunities for tax evasion. The government’s medium-term tax strategy, as outlined by the Organization for Investment Economic and Technical Assistance of Iran, anticipates continued alignment of indirect tax policy with macroeconomic stabilization and digital transformation objectives through 2027.

Enforcement, Penalties, and Audit Trends

Enforcement of tax law in Iran has intensified in recent years, reflecting the government’s efforts to increase non-oil revenues and enhance fiscal transparency. The Iranian National Tax Administration (INTA) is the principal agency responsible for tax enforcement, audit, and collection. Its mandate covers the administration of direct taxes, value added tax (VAT), and the oversight of compliance with evolving tax regulations.

In terms of enforcement, INTA has expanded the scope and sophistication of its audit activities. Since 2022, the agency has increasingly utilized digital systems to cross-reference taxpayer information, employing data analytics to identify discrepancies and underreporting. The 2025 budget law anticipates continued investments in electronic tax administration, with a focus on linking databases from banks, customs, and property registries to facilitate comprehensive taxpayer profiling (Iranian National Tax Administration).

Penalties for non-compliance with tax obligations in Iran are governed by the Direct Taxation Act and the VAT Law. Common infractions include late filing, underreporting income, failure to register, and non-payment of taxes. For example, late filing of tax returns can result in fines of up to 30% of the unpaid tax, while intentional evasion may trigger criminal prosecution and substantial financial penalties. Amendments in recent years have increased the severity of penalties, especially for repeat offenders and those engaged in large-scale tax evasion (Islamic Parliament Research Center of the Islamic Republic of Iran).

Audit trends reveal that INTA has shifted its focus toward high-risk sectors, including real estate, import/export businesses, and professionals with high income potential. The number of audits conducted annually has risen, with over 200,000 corporate and individual audits reported in the last fiscal year. Digitalization of audit processes is expected to further increase audit coverage and reduce opportunities for tax evasion in 2025 and beyond (Iranian National Tax Administration).

Looking ahead, compliance is likely to become more demanding for Iranian businesses and individuals. The ongoing integration of tax, banking, and customs data is projected to improve detection of unreported income and cross-border transactions. The government’s revenue strategy for 2025 and subsequent years prioritizes greater efficiency in tax collection and stricter enforcement, suggesting that taxpayers will face heightened scrutiny and potentially stiffer penalties for non-compliance (Ministry of Economic Affairs and Finance).

Sector-Specific Impacts: Energy, Technology, and Startups

Iran’s tax law landscape in 2025 continues to shape sector-specific outcomes, particularly for the energy, technology, and startup sectors. Each sector faces nuanced compliance requirements and tax incentives, reflecting the government’s dual aims of boosting revenues and fostering targeted economic growth.

- Energy Sector: As Iran’s most significant economic pillar, the energy sector—especially oil and gas—remains subject to heavy taxation and close regulatory oversight. The Iranian National Tax Administration (INTA) enforces robust tax compliance, with the 2025 budget maintaining a special windfall tax on crude exports and continued focus on tax base broadening. For example, the 2025 budget law sustains the corporate tax rate at 25% for energy companies, with additional surcharges on high-revenue extractive activities. The government is also intensifying audits and digital reporting to counteract evasion, as outlined by Ministry of Petroleum and INTA directives.

- Technology Sector: The technology sector enjoys several exemptions and incentives to stimulate innovation and digital transformation. According to INTA, IT firms registered with the Science and Technology Park system can benefit from up to 15 years of tax holidays, provided they meet criteria regarding R&D investment and domestic value creation. The 2025 tax reforms have expanded the digital economy’s tax base, targeting e-commerce platforms and digital services for VAT registration and electronic invoicing, in line with the E-Government roadmap set forth by the Ministry of Information and Communications Technology.

- Startups: The startup ecosystem continues to receive favorable tax treatment to nurture entrepreneurship. Startups certified by the Vice Presidency for Science and Technology are eligible for several years of income tax exemption, as per the 2025 extension of the Knowledge-Based Companies Law. However, compliance requirements are growing stricter: startups must fully digitize accounting, participate in the national e-invoicing scheme, and regularly report financials—measures enforced by INTA to enhance transparency and prevent abuse.

Key statistics for the current year indicate that tax revenues from the energy sector are projected to account for over 35% of total tax income, while the technology and startup sectors contribute a growing but still modest share (INTA). For 2025 and beyond, the outlook is for continued tightening of compliance, wider digitalization, and gradual reduction of blanket exemptions, as the government seeks to broaden the tax base amid fiscal pressures. Sectoral tax policies are likely to further differentiate, balancing revenue needs with economic diversification goals.

Future Outlook: Projected Reforms Through 2029

Iran’s tax law has been undergoing a series of reforms, with accelerating momentum expected through 2029, as policymakers seek to modernize the system, broaden the tax base, and reduce reliance on oil revenues. The government’s strategic direction is outlined in the Sixth and Seventh Five-Year Development Plans, which emphasize fiscal sustainability and increased tax-to-GDP ratios. In 2025 and the following years, several key initiatives and changes are forecasted to shape Iran’s tax landscape.

- Digitalization and Automation: The Iranian National Tax Administration (INTA) is actively implementing comprehensive digitalization of tax processes. This includes expanding electronic tax declarations, e-invoicing, and the use of data analytics for compliance monitoring. The goal is to reduce tax evasion, improve efficiency, and enhance taxpayer services by 2026-2027 Iranian National Tax Administration.

- Broadening the Tax Base: Policymakers are working to reduce exemptions and bring more economic activities, particularly in the shadow economy, under the tax net. Legislative proposals targeting real estate speculation, luxury goods, and digital platforms are anticipated, in line with national strategies to increase non-oil revenues Islamic Consultative Assembly.

- VAT and Indirect Tax Reforms: There is an expected gradual increase in the Value Added Tax (VAT) rate, currently at 9%, alongside efforts to streamline VAT refunds and close loopholes. The government aims to harmonize indirect taxes and align them more closely with international standards by 2028 Iranian National Tax Administration.

- International Cooperation and Anti-Avoidance: Iran is continuing to enhance its anti-money laundering (AML) and tax information exchange frameworks, seeking closer alignment with global practices. Ongoing negotiations for mutual administrative assistance in tax matters and implementation of anti-avoidance measures are expected to gain traction through 2029 Central Bank of the Islamic Republic of Iran.

- Compliance and Enforcement: There is a clear trend toward stricter enforcement, including increased audits, use of data-matching technologies, and higher penalties for non-compliance. The INTA has stated its intention to focus enforcement resources on high-risk sectors and large taxpayers Iranian National Tax Administration.

According to INTA, tax revenue collection increased by more than 50% in fiscal year 2023-2024, and the government projects continued double-digit growth rates as reforms take effect. Looking ahead, further legislative amendments, capacity building, and public awareness campaigns are expected to be central to achieving fiscal targets and ensuring compliance Iranian National Tax Administration. The outlook through 2029 is for a more transparent, efficient, and robust tax system, though challenges remain in execution and stakeholder adaptation.

Official Resources and Guidance for Compliance (e.g., intamedia.ir, tax.gov.ir)

Iran’s tax system has undergone significant reforms in recent years, with an emphasis on digitalization, transparency, and broadening the tax base. For taxpayers and professionals seeking up-to-date guidance and compliance support, several official government resources are central to navigating the evolving tax landscape in 2025 and beyond.

-

Iranian National Tax Administration (INTA):

The Iranian National Tax Administration (INTA) is the principal authority overseeing tax collection, enforcement, and interpretation of tax law in Iran. INTA’s official portal provides comprehensive information on current tax laws, executive instructions, circulars, and frequently asked questions. It also hosts digital services for tax return filing, taxpayer registration, and online payment systems, supporting compliance with the latest regulations. -

Tax Electronic Services Portal:

The Tax Electronic Services Portal serves as INTA’s main digital infrastructure for taxpayers. Through this portal, individuals and legal entities can submit tax declarations, access their tax accounts, track correspondence, and receive notifications about deadlines and legal changes. The portal’s expansion is part of the government’s ongoing initiative to reduce manual processes and enhance compliance through automation. -

Official Announcements and Legislative Updates:

All official amendments to tax law, including recent changes such as the implementation of the VAT Law reforms and updates to direct tax regulations, are published on INTA’s website. The Iranian National Tax Administration regularly issues guidance, executive orders, and explanatory notes—critical for professionals tracking compliance obligations as legislative reforms continue into 2025. -

Support and Dispute Resolution:

INTA provides dedicated support channels through its online platforms, including helplines and inquiry forms. For complex compliance or dispute resolution matters, taxpayers can find procedures for appeals, requests for tax reviews, and access to relevant legal forms via the Tax Electronic Services Portal. -

Statistical Reports and Compliance Data:

Annual reports and key statistics on tax collection, audit outcomes, and sectoral compliance are published by INTA, offering transparency and benchmarking for taxpayers. These reports inform policy outlook and compliance trends for upcoming years.

Staying informed through these official resources is essential for individuals and businesses in Iran to navigate evolving tax requirements, avoid penalties, and benefit from government guidance as tax law reforms accelerate toward 2025 and beyond.