Table of Contents

- Overview of the Saint Lucia Tax System (2025 Edition)

- Key Tax Rates and Brackets for Individuals and Businesses

- Recent Legislative Changes Impacting Taxes in Saint Lucia

- Tax Compliance: Filing Requirements and Deadlines

- VAT, Customs Duties, and Indirect Taxes Explained

- International Taxation and Double Tax Agreements

- Incentives, Exemptions, and Special Regimes

- Common Pitfalls and Audit Triggers for Taxpayers

- Future Outlook: Predicted Changes for 2026–2029

- Official Resources and Guidance for Staying Updated

- Sources & References

Overview of the Saint Lucia Tax System (2025 Edition)

Saint Lucia’s tax system in 2025 is characterized by a mix of direct and indirect taxes, administered primarily by the Inland Revenue Department (IRD) and the Customs & Excise Department. The tax regime is guided by the Income Tax Act, the Value Added Tax Act, and various sector-specific legislation, reflecting ongoing efforts to improve compliance and broaden the tax base.

Key Tax Types and Rates (2025)

- Personal Income Tax: Residents are subject to a progressive income tax, with rates ranging up to 30% for individuals. Personal allowances and deductions apply, including those for dependents and certain expenditures.

- Corporate Income Tax: The standard corporate tax rate stands at 30%. Incentives and reduced rates apply to specific sectors, particularly in tourism, manufacturing, and international financial services, under the Investment Incentives Act.

- Value Added Tax (VAT): VAT is levied at a general rate of 12.5% for most goods and services, with a reduced rate of 10% for hotels and the accommodation sector. Some items are zero-rated or exempt, notably basic food items and selected financial services.

- Withholding Tax: A 10% withholding tax applies to certain payments to non-residents, including dividends, interest, and royalties.

- Property and Excise Taxes: Annual property taxes are assessed based on market value, while excise duties are imposed on specific imports such as alcohol, tobacco, and petroleum products.

Compliance and Administration

The IRD has prioritized digital transformation, with electronic filing and payment systems now mandatory for most businesses. Compliance drives have been intensified, targeting both underreporting and non-registration, especially in the shadow economy. Penalties for non-compliance include fines, interest, and potential legal action, as outlined in the Income Tax Act and Regulations.

Key Statistics and Outlook (2025 and Beyond)

Tax revenue accounts for approximately 25% of Saint Lucia’s GDP, with VAT and income taxes comprising the largest shares. The government’s 2025 budget projects a modest increase in tax receipts, driven by economic recovery and improved compliance strategies (Ministry of Finance). Looking ahead, authorities are expected to continue modernizing tax administration, enhance cross-border cooperation to reduce evasion, and review incentives to align with international standards. As Saint Lucia balances fiscal pressures and economic growth, ongoing reforms aim to ensure a fair, efficient, and sustainable tax environment.

Key Tax Rates and Brackets for Individuals and Businesses

Saint Lucia’s tax landscape in 2025 continues to be governed by the Inland Revenue Department under the Income Tax Act and its subsidiary regulations. The system is characterized by progressive personal income tax rates, a standard corporate income tax, and a value-added tax (VAT) regime. Recent years have seen a stabilization of rates, though incremental changes may occur as part of ongoing fiscal reforms.

-

Personal Income Tax: For the 2025 assessment year, residents are taxed on their worldwide income using a progressive scale. As of the latest schedules:

- 0% for annual income up to XCD 18,400

- 10% for income between XCD 18,401 and XCD 25,000

- 15% for income between XCD 25,001 and XCD 30,000

- 20% for income between XCD 30,001 and XCD 50,000

- 30% for income above XCD 50,000

These brackets have remained consistent since the last adjustment in previous fiscal years, with no major rate changes announced for 2025 (Inland Revenue Department).

- Corporation Tax: Resident companies are subject to a flat corporate income tax rate of 30% on worldwide profits. Non-resident companies are taxed at the same rate on income sourced within Saint Lucia. Certain incentives and exemptions are available for businesses engaged in priority sectors, as outlined by the Invest Saint Lucia.

- Value-Added Tax (VAT): Saint Lucia levies a standard VAT rate of 12.5% on most goods and services, with a reduced rate of 10% applicable to hotels and the accommodation sector. Some basic commodities and essential services are zero-rated or exempt (Inland Revenue Department).

-

Other Key Taxes:

- Withholding Tax: 10% on payments to non-residents for dividends, interest, royalties, and management fees.

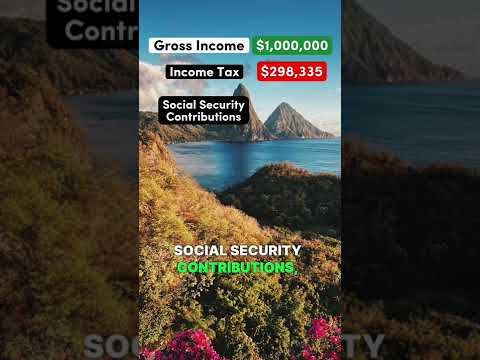

- Social Security Contributions: Employers contribute 5% and employees 5% of gross salaries, capped at a maximum insurable earnings threshold (Saint Lucia National Insurance Corporation).

Looking forward, Saint Lucia’s tax regime is expected to remain broadly stable through the next few years, with incremental reforms focused on compliance, digitalization of tax administration, and targeted incentives to stimulate investment and economic resilience (Ministry of Finance, Economic Development and the Youth Economy).

Recent Legislative Changes Impacting Taxes in Saint Lucia

In recent years, Saint Lucia has enacted several legislative changes impacting its tax landscape, reflecting the nation’s commitment to international standards and efforts to enhance fiscal sustainability. The Income Tax (Amendment) Act 2023, which took effect in January 2024, introduced a new personal income tax regime. Notably, the standard personal income tax rate remains at 30%, but the legislation has broadened the tax base by adjusting exemptions and deductions, aiming to increase domestic tax compliance and revenue mobilization. Changes also included updates to the definition of taxable income and the streamlining of personal allowances, aligning with recommendations from the Government of Saint Lucia.

On the corporate front, the Corporate Income Tax (CIT) rate remains at 30%, but the government has implemented stricter transfer pricing rules and bolstered anti-avoidance provisions in accordance with global tax transparency initiatives. These were introduced through amendments to the Income Tax Act and supporting regulations in 2023 and 2024, reflecting Saint Lucia’s commitment to meeting the standards set by the OECD Base Erosion and Profit Shifting (BEPS) Project. These measures are particularly relevant for international business companies and financial sector entities operating in or through Saint Lucia.

The Value Added Tax (VAT) system has also seen refinement. The VAT standard rate remains at 12.5% for most goods and services, while the reduced rate of 0% continues to apply to certain basic food items and essential services. However, as part of the 2024 Budget, scope adjustments for VAT-exempt and zero-rated goods were enacted, designed to optimize revenue collection while protecting vulnerable groups. These changes are detailed in the 2024/2025 Appropriations Bill and the VAT (Amendment) Act, as published by the Inland Revenue Department of Saint Lucia.

In the realm of international compliance, Saint Lucia has continued to enhance its Anti-Money Laundering (AML) and Common Reporting Standard (CRS) frameworks, with updates to the Financial Services Regulatory Authority Act and more robust exchange-of-information protocols in 2024. These efforts reflect ongoing cooperation with the OECD and the Caribbean Financial Action Task Force.

Looking ahead to 2025 and beyond, Saint Lucia’s legislative agenda signals further alignment with international tax transparency, ongoing digitalization of tax administration, and continued adjustments to tax incentives to balance competitiveness with fiscal responsibility. These trends are expected to shape the compliance environment and the investment climate in the coming years.

Tax Compliance: Filing Requirements and Deadlines

Saint Lucia’s tax compliance framework in 2025 is governed by the Income Tax Act (Chapter 15.02) and administered by the Inland Revenue Department (IRD) under the Ministry of Finance. Individuals and companies resident in Saint Lucia are subject to income tax on their worldwide income, while non-residents are taxed only on income sourced within the country. Compliance with tax obligations is a legal requirement, with specific deadlines and procedures enforced for timely filing and payment.

-

Personal Income Tax: Resident individuals must file an annual income tax return if their annual income exceeds the statutory threshold, which for 2025 remains at XCD 18,000. The filing deadline for individuals is March 31 of the year following the assessment year (i.e., March 31, 2026 for the 2025 tax year). Returns must be filed using the prescribed forms, either electronically through the IRD’s e-filing portal or in person at the IRD offices. Payment of any tax due is required by the same deadline to avoid penalties.

Inland Revenue Department -

Corporate Income Tax: Companies incorporated or effectively managed in Saint Lucia are required to file an annual corporate income tax return. The standard tax rate remains at 30%. The filing deadline is three months after the close of the company’s financial year (for most companies, by March 31 if the fiscal year aligns with the calendar year). Estimated tax payments are required in three installments during the assessment year, with the final balance due upon filing.

Inland Revenue Department -

Value-Added Tax (VAT): Businesses with annual taxable supplies exceeding XCD 400,000 must register for VAT. VAT returns are due on the 21st day of the month following the end of each tax period (monthly or quarterly, depending on turnover). Prompt filing and payment of VAT are mandatory to avoid interest and penalties.

Value Added Tax Department -

Other Compliance Obligations: Employers are responsible for monthly PAYE (Pay As You Earn) withholding and remittance, due by the 15th of the following month. Withholding tax on non-resident payments, if applicable, must also be remitted promptly.

Inland Revenue Department

The IRD is actively modernizing compliance systems, including expanded e-filing capabilities and increased taxpayer education. For 2025 and beyond, continued digitalization and stricter enforcement are expected, with penalties for non-compliance including fines, interest, and potential prosecution. Taxpayers are advised to monitor official updates for changes to thresholds, rates, or deadlines.

Ministry of Finance, Economic Development and Youth Economy

VAT, Customs Duties, and Indirect Taxes Explained

Saint Lucia’s tax regime relies significantly on indirect taxation, with Value Added Tax (VAT) and customs duties forming the backbone of government revenue. First introduced in 2012, VAT is governed by the Value Added Tax Act, Cap. 15.25, and remains a key fiscal instrument in 2025. The standard VAT rate is 12.5% for most goods and services, with a reduced rate of 10% applicable to the hotel sector, and zero-rating or exemption for select essential items and services, including basic foodstuffs and certain financial services (Inland Revenue Department, Saint Lucia).

Compliance with VAT obligations requires businesses with annual taxable supplies exceeding XCD 180,000 to register, file monthly returns, and remit collected tax. The Inland Revenue Department has increased digitalization of processes, offering e-filing and payment portals to improve compliance and efficiency. Failure to comply attracts penalties, interest, and potential prosecution, underscoring the need for rigorous internal controls.

Customs duties are regulated under the Customs (Control and Management) Act and the Harmonized Commodity Description and Coding System. Typical rates range from 0% on essential imports to 40% on luxury items, with agricultural products, alcohol, and tobacco often subject to higher bands. In addition, Excise Tax applies to specific goods such as fuel, motor vehicles, and tobacco. The Customs & Excise Department is responsible for the administration, assessment, and collection of these duties, with strict border controls and post-clearance audits to ensure accurate declaration and duty payment.

Indirect tax collections have shown resilience, contributing over 60% of Saint Lucia’s total tax revenues in recent years (Ministry of Finance, Saint Lucia). The government periodically reviews the VAT base and customs tariff schedules to align with fiscal policy objectives and regional trade obligations under CARICOM. In 2025, ongoing consultations are underway regarding further digital transformation and the possible adjustment of VAT thresholds to broaden the tax net and address compliance gaps.

Looking ahead, sustained efforts to strengthen tax administration are expected, with a focus on real-time data analytics, risk-based audits, and enhanced taxpayer education. These measures aim to bolster revenue mobilization while simplifying compliance for taxpayers and supporting Saint Lucia’s broader economic development goals.

International Taxation and Double Tax Agreements

Saint Lucia’s approach to international taxation and double tax agreements (DTAs) is shaped by its status as an offshore financial center and a member of the Organisation of Eastern Caribbean States (OECS). The country’s tax framework is designed to encourage foreign investment while adhering to international standards on tax transparency and anti-avoidance measures.

As of 2025, Saint Lucia does not have an extensive network of double tax agreements. The country has signed a limited number of DTAs, including a notable agreement with the United Kingdom to prevent double taxation and fiscal evasion with respect to taxes on income and capital gains. This agreement facilitates cross-border investment by reducing the risk of double taxation for residents and companies operating in both jurisdictions, and it provides mechanisms for resolving tax disputes and exchanging information between authorities (HM Revenue & Customs).

Saint Lucia is also a signatory to the Multilateral Convention on Mutual Administrative Assistance in Tax Matters, which enhances cooperation among tax authorities globally in the exchange of information, recovery of taxes, and other forms of administrative assistance (Organisation for Economic Co-operation and Development). The country’s participation in this convention aligns with international efforts to combat tax evasion and increase transparency.

To comply with global standards, Saint Lucia has adopted the Common Reporting Standard (CRS) for the automatic exchange of financial account information and is a participant in the OECD’s Base Erosion and Profit Shifting (BEPS) Inclusive Framework. These measures require financial institutions to report information on foreign account holders, which is then shared with the relevant tax authorities, thus increasing compliance requirements for both individuals and companies with international dealings (Inland Revenue Department, Saint Lucia).

Recent legislative updates have focused on strengthening anti-avoidance laws and refining transfer pricing rules to prevent profit shifting by multinational enterprises. Compliance obligations for international businesses are becoming more rigorous, including the need to provide documentation supporting the arm’s length nature of cross-border transactions.

Looking ahead, Saint Lucia is expected to continue expanding its treaty network and refining its legal infrastructure to meet evolving international tax standards. This is part of a broader strategy to sustain its attractiveness as an investment destination while ensuring it remains off tax blacklists and maintains access to global financial markets.

Incentives, Exemptions, and Special Regimes

Saint Lucia offers a range of tax incentives, exemptions, and special regimes aimed at fostering investment, supporting key industries, and promoting economic development. The current framework is shaped by legislations such as the Investment Incentives Act and the Fiscal Incentives Act, both administered by the Ministry of Finance and the Inland Revenue Department.

- Corporate Tax Exemptions: Businesses meeting certain criteria—especially in manufacturing, agriculture, and tourism—may qualify for full or partial exemptions from corporate income tax for up to 15 years. The duration and extent depend on factors such as indigenous ownership, export orientation, and capital investment levels.

- Import Duty and VAT Relief: Approved enterprises under the Fiscal Incentives Act and Ministry of Finance may benefit from exemptions or reductions in import duties, excise taxes, and Value Added Tax (VAT) on machinery, equipment, raw materials, and select inputs necessary for their operations.

- Tourism Incentives: The Tourism Incentives Act grants concessions to hotels and tourism-related projects, including duty-free importation of building materials and furnishings, as well as income tax holidays of up to 15 years, to stimulate continued growth in this vital sector.

- Special Economic Zones (SEZ): The government has signaled intent to expand SEZs to attract foreign direct investment in logistics, manufacturing, and technology. Businesses in SEZs may receive tailored tax holidays, streamlined customs procedures, and other regulatory exemptions, although details for 2025 onward are being finalized.

- Global Business Companies (GBC): Saint Lucia’s Financial Services Regulatory Authority administers special regimes for international business companies and trusts. GBCs are subject to a competitive corporate tax rate (as low as 1%) or may elect tax exemptions, provided they do not conduct business locally.

Compliance with these incentives requires strict adherence to reporting and eligibility requirements. The Inland Revenue Department conducts periodic audits to ensure proper use of concessions. Recent statements by the Ministry of Finance indicate ongoing review of incentive schemes to align with international standards and curb potential abuse, in line with recommendations from the OECD’s Base Erosion and Profit Shifting (BEPS) framework.

As Saint Lucia continues to balance revenue needs with investment promotion, expect further refinement of tax incentives and increased compliance monitoring in 2025 and beyond.

Common Pitfalls and Audit Triggers for Taxpayers

Saint Lucia’s tax system, administered by the Inland Revenue Department (IRD), is governed by several laws, including the Income Tax Act and the Value Added Tax (VAT) Act. For 2025 and the near-term horizon, taxpayers—both individuals and businesses—should be aware of common pitfalls that can lead to audits or penalties.

- Underreporting of Income: Failure to fully disclose all sources of income remains one of the most frequent triggers for tax audits. This includes income from rental properties, overseas assets, freelance work, and side businesses. The IRD has increased cross-checks using third-party data from banks and property registries, making non-disclosure riskier than before (Inland Revenue Department).

- Incorrect VAT Returns: VAT-registered businesses must strictly adhere to the timely and accurate filing of VAT returns. Common errors include misclassification of zero-rated and exempt supplies, failure to properly account for input tax credits, and missed deadlines. The IRD’s e-filing platform tracks irregularities and late submissions, often flagging these for further review (Inland Revenue Department).

- Improper Record Keeping: Taxpayers are required by law to maintain detailed accounting records for at least six years. Missing or incomplete records raise red flags during routine compliance checks and are a frequent cause of audits and adjustments (Inland Revenue Department).

- Failure to Withhold or Remit Taxes: Employers and payers of certain types of income (such as dividends or interest) are required to withhold taxes at source and remit them to the IRD. Non-compliance, whether through oversight or deliberate evasion, can result in significant penalties and is a top audit trigger.

- Late or Non-Filing: Both individuals and businesses must file annual returns by statutory deadlines—generally March 31 for individuals and within three months of year-end for companies. Chronic late filers or non-filers are subject to penalty assessments and increased scrutiny.

The IRD has signaled ongoing enhancements in digital compliance tools and data analytics, increasing the likelihood of detection for non-compliance. For 2025 and beyond, Saint Lucia is expected to further align with international standards on tax transparency and information sharing, particularly under the OECD’s Common Reporting Standard. Taxpayers should prioritize accurate, timely filings and robust record-keeping to avoid costly audits and penalties (Inland Revenue Department).

Future Outlook: Predicted Changes for 2026–2029

Looking ahead to the period 2026–2029, Saint Lucia’s tax landscape is expected to evolve in response to both domestic policy objectives and international pressures. The government has signaled intentions to further modernize the tax system, enhance compliance, and align with global standards, especially in areas such as anti-money laundering, transparency, and digital tax administration. Key legislative priorities are likely to focus on broadening the tax base, improving efficiency, and ensuring fiscal sustainability.

- Corporate and Personal Income Tax Reforms: Ongoing assessments by the Inland Revenue Department suggest a review of existing rates and allowances to maintain competitiveness while securing sufficient revenue. With Saint Lucia’s standard corporate income tax at 30% and personal income tax rates peaking at 30%, policymakers are examining potential restructuring to attract investment and balance social needs.

- VAT System Enhancements: The Value Added Tax (VAT), currently levied at a standard rate of 12.5% (with some goods and services exempt or zero-rated), is under continual review. The Government of Saint Lucia has indicated interest in streamlining VAT administration and reducing compliance gaps, leveraging new technology and data analytics to improve collection and reduce evasion.

- International Tax Compliance: Saint Lucia remains committed to meeting the obligations of the OECD's BEPS (Base Erosion and Profit Shifting) framework and complying with the Common Reporting Standard. Further legislative updates are expected to address tax transparency, beneficial ownership reporting, and the prevention of harmful tax practices, particularly concerning offshore structures and investment programs.

- Digitalization of Tax Administration: The Inland Revenue Department is investing in digital platforms for tax filing, payments, and taxpayer services. Full implementation is anticipated by 2027, which should enhance compliance, reduce administrative burdens, and provide real-time analytics for policy adjustments.

- Citizenship by Investment Programme: Tax aspects of Saint Lucia’s popular Citizenship by Investment Programme may face tighter regulation and reporting requirements as international scrutiny increases, particularly around source of funds and tax residency rules.

Key statistics from the Inland Revenue Department indicate that tax revenues comprised approximately 23% of GDP in 2023, and the government aims to incrementally increase this ratio through improved compliance and economic growth. The outlook for 2026–2029 is characterized by ongoing modernization, global alignment, and the pursuit of fiscal resilience, with stakeholders advised to monitor legislative updates and prepare for enhanced reporting and compliance standards.

Official Resources and Guidance for Staying Updated

Staying current with Saint Lucia’s tax laws and compliance requirements is essential for individuals and businesses operating in the jurisdiction. The government provides several official resources and support channels to help taxpayers remain informed about legislative changes, filing deadlines, and procedural updates for 2025 and beyond.

- Inland Revenue Department (IRD): The Inland Revenue Department is the principal authority for tax collection and administration in Saint Lucia. Its website offers downloadable forms, guides, updates on tax rates, and the latest information on Value Added Tax (VAT), income tax, property tax, and compliance procedures. The IRD also issues public notices about legislative amendments and upcoming deadlines.

- Government of Saint Lucia Online Portal: The central government portal, Government of Saint Lucia, aggregates official publications, press releases, and links to laws and regulatory bodies. Taxpayers will find legislative updates, budget statements, and key policy announcements relevant to taxation.

- Legal Framework and Laws: The full text of tax-related statutes, including the Income Tax Act, VAT Act, and other fiscal legislation, is available through the Government of Saint Lucia—Legislation page. This resource is critical for understanding statutory obligations and recent amendments.

- Professional Bodies: The Institute of Chartered Accountants of the Caribbean (ICAC) and the Saint Lucia Institute of Chartered Accountants (SLICA) provide guidance, updates, and resources for tax professionals, including best practices for compliance and details on continuing professional education.

- Direct Contact and Support: The IRD maintains helpdesks, contact emails, and phone support for taxpayer queries. Taxpayers can schedule appointments or submit inquiries for clarifications on compliance requirements, electronic filing, and payment options directly through the Inland Revenue Department Contact Page.

To ensure ongoing compliance through 2025 and anticipate future changes, taxpayers are encouraged to regularly consult these official channels, subscribe to government notifications, and engage with recognized professional bodies for the most authoritative guidance on Saint Lucia’s evolving tax landscape.